What is a genuine secondment using an A1 certificate?

In an increasingly global workforce, businesses regularly send employees to work temporarily in other countries. When that happens within Europe, one key concept determines whether the arrangement is compliant: genuine secondment, supported by an A1 certificate.

This is not just essential for HR teams, but for any organisation managing cross-border work.

Understanding the A1 certificate

An A1 certificate is an official document confirming which country’s social security system applies to an employee working across borders.

Put simply, it proves that even though an employee is working in another country, they remain insured and continue to pay social security in their home country.

Without an A1 certificate, the default rule applies, whereby social security contributions are paid in the country where the work is performed.

This can create immediate obligations in the host country, even for short assignments.

We have also explained in a previous blog here – that A1 certificates solely relate to Social Security obligations and not income tax.

What is a secondment?

A secondment, often referred to as a ‘posting’, occurs when an employee is sent temporarily by their employer to work in another country, while remaining employed by the original organisation. The key point to consider, is that the employer must have had a pre-existing employment relationship with the employee prior to the secondment.

This is one of the most common scenarios in which an A1 certificate is required. However, not all secondments are considered “genuine” by regulators.

So, what constitutes a “genuine” secondment?

It is not just about sending someone abroad; it must also meet specific legal criteria under EU social security rules. According to Regulation (EC) No. 883/2004, a valid secondment supported by an A1 form typically requires:

- Temporary duration: the assignment must be time-limited, generally up to 24 months.

- An ongoing employment relationship: there must be a direct relationship between the employee and the home employer throughout the assignment.

This means:

- The original employer retains control

- The employment contract remains in place

- The employee is not “transferred” to the host entity

- Work is performed on behalf of the home employer: the employee must continue to work for the sending company and cannot be effectively hired by the host organisation.

- No replacement of another Posted Worker: the role must not be filling a rotating or ongoing position intended to circumvent local regulations.

Why the A1 Certificate is central to a genuine secondment

The A1 certificate is what legally validates the secondment. It informs the host country’s authorities that: “This worker is already covered by another social security system, so no local contributions are due.”

This has several important effects:

- Prevents double social security contributions

- Ensures continuous coverage (pensions, healthcare, unemployment benefits, etc.)

- Provides proof during inspections or audits

Without it, companies risk:

- Backdated contributions in the host country

- Penalties and compliance issues

- Gaps in employee coverage

Genuine vs Non-Genuine Secondments

One of the key compliance risks is assuming that any international assignment qualifies as a secondment.

Genuine Secondment (Compliant)

- Temporary and clearly defined

- The employee remains tied to their home employer

- A1 certificate obtained before work begins

- Social security continues in the home country

Non-Genuine Secondment (Risky)

- Long-term or indefinite assignment

- The employee is effectively integrated into the host company

- No real link to the home employer

- No A1 certificate (or conditions not met)

In these cases, the host country may require local social security registration from day one.

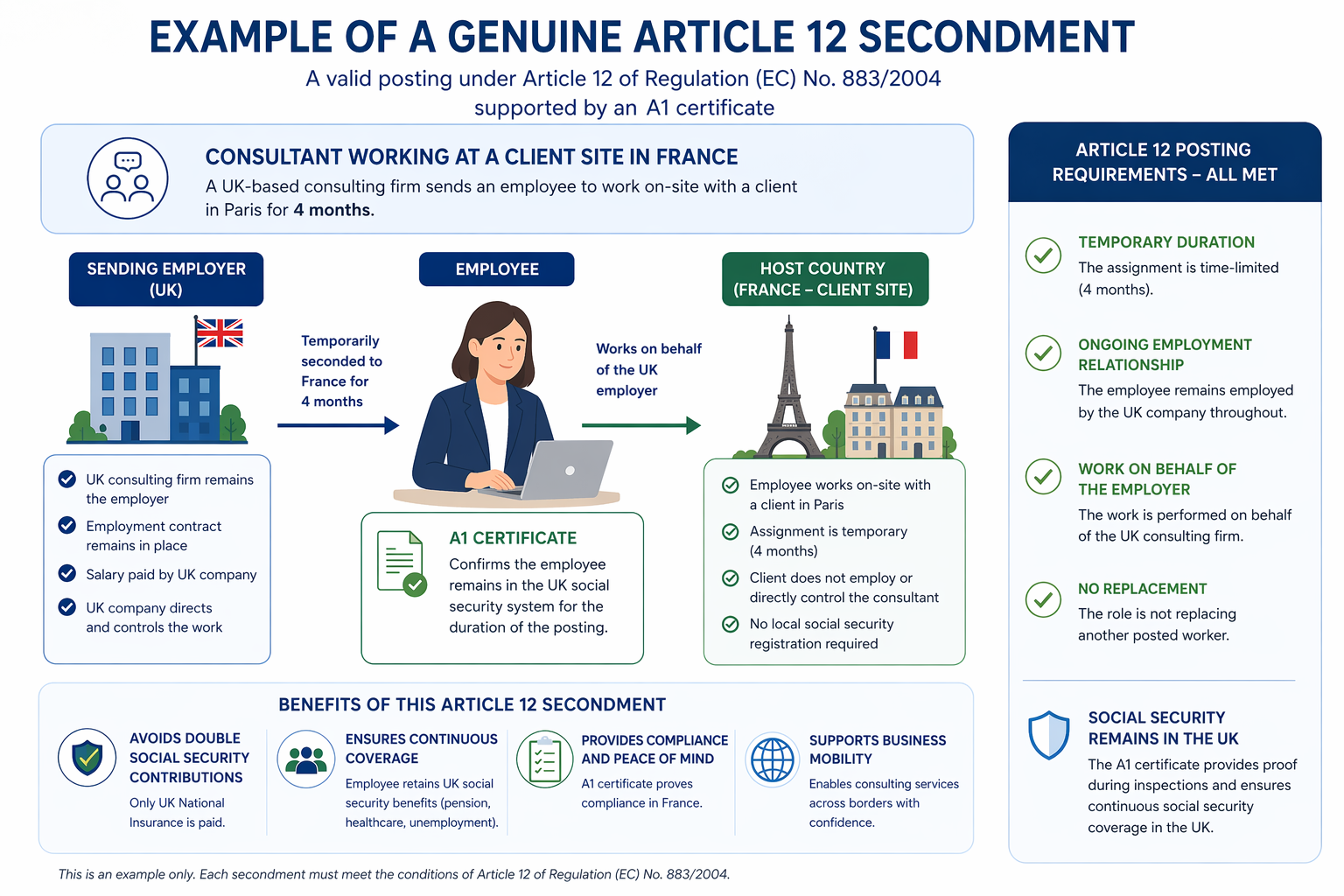

Example of an Article 12 Secondment

Scenario: Consultant working at a client site in France.

A consulting firm in the UK sends an employee to work on-site with a client in Paris for 4 months.

- The consultant remains employed and managed by the UK firm

- The work is delivered on behalf of the UK employer

- The client does not employ or directly control the consultant

Outcome: This qualifies as an Article 12 posting, provided the relationship clearly remains with the UK employer. An A1 certificate applies.

We have also included a visual representation of this scenario below.

Common Misunderstandings

Many organisations do not realise when an A1 certificate is required. In reality:

- It applies even to short business trips or meetings

- It is triggered by where the work is physically performed, not where the company is based

- It covers social security only, not tax, immigration, or employment law

A genuine secondment involves more than just sending an employee abroad, it’s a legally structured arrangement backed by an A1 certificate.

Get it right and your business will benefit from:

- Seamless cross-border working

- Clear compliance

- Protected employees

Get it wrong, however, and the consequences can include double contributions, fines, and regulatory scrutiny. In today’s mobile workforce, it’s not just helpful to understand the relationship between secondments and A1 certificates – it’s essential.